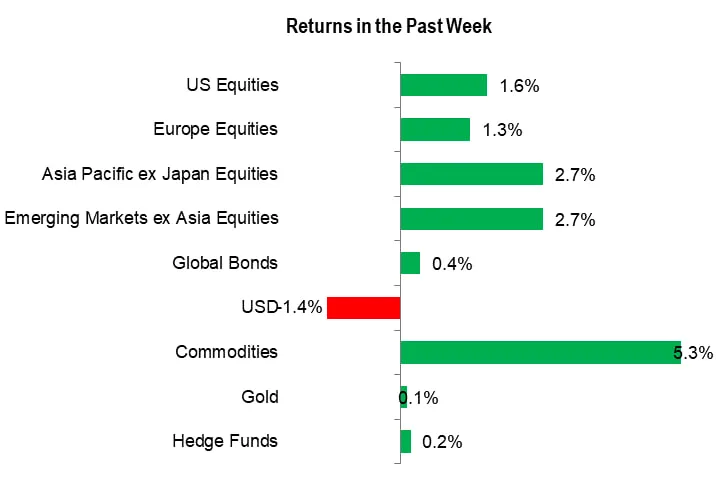

Over the course of the week, various stock market indices experienced notable gains. The MSCI All Country World index rose by 0.6%, while the S&P 500 and Nasdaq 100 indices saw jumps of 2.6% and 3.8%, respectively. Additionally, the German DAX 40 advanced by 2.5% and the UK FTSE 100 rose by 1.0%. In Asia, the Hang Seng index rose by 3.3% and Japan’s Nikkei 225 experienced a significant surge of 4.5%. Within the realm of currency exchange rates, risk-sensitive currencies such as the Australian dollar and New Zealand dollar rose by approximately 1.9% and 1.7%, respectively, throughout the week.